🗓️ 2025 Mid-Year Review · Part I

A Volatile Half-Year Marked by Structural Shifts

📝 Editor’s Note:

This 2025 Mid-Year Review is presented in two parts.

Part I (this issue) provides a global macro and investment overview, including key asset classes and market themes. All data is current as of 6 June 2025.

Part II (coming next) will dive into regional market performance across the US, UK, and China, followed by investment outlooks for the second half of the year.

🔍 Macro Overview

The first half of 2025 has been defined by heightened tension and structural realignments across global markets.

Global trade took a sharp turn inward following the Trump administration’s sweeping tariff hikes, starting in February. These measures targeted China, the Middle East, and several Western allies, tightening trade conditions worldwide.

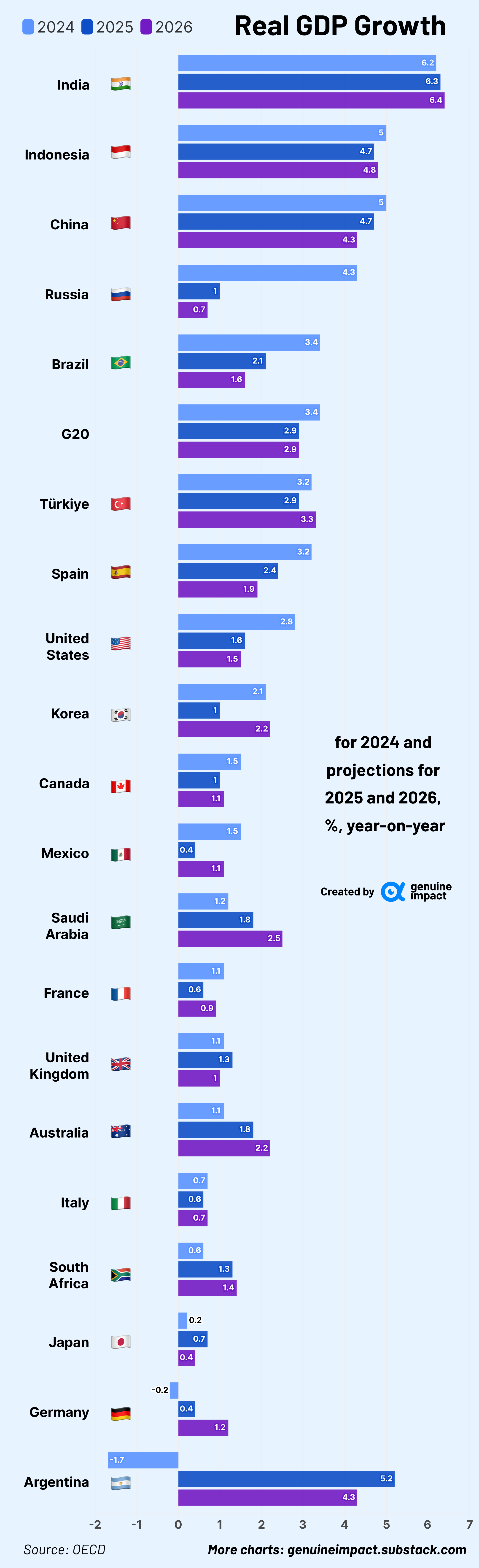

Reflecting the impact of these policies, the OECD now expects global GDP growth to slow from 3.3% in 2024 to just 2.9% this year and next — with the 🇺🇸United States, 🇨🇦Canada, 🇲🇽Mexico, and 🇨🇳China bearing the brunt of the deceleration. By the fourth quarter of 2025, global output is projected to grow only 2.6% year-on-year, with U.S. growth plunging to a mere 1.1%.

Meanwhile, defence spending surged. In May, the U.S. State Department approved billions of dollars in new arms deals. Across Europe, national defence strategies were reinforced — the UK, for instance, unveiled its 2025 Strategic Defence Review, pledging to raise defence spending to 2.5% of GDP by 2027.

🌍 Global Investment Landscape: Flight to Safety Amid Fragmentation

Markets in H1 2025 reflected deep divergence, shaped by macro policy shocks and alternating waves of risk aversion.

Commodities saw a strong start, buoyed by solid fundamentals. But February's tariff escalation triggered broad sell-offs in risk assets, driving capital into safe-haven plays like gold and Bitcoin.

By April, commodities saw a $57B net outflow, while gold ETF inflows neared 2022's war-time highs.

After the U.S. and China agreed to a partial tariff easing deal in May, investor sentiment rebounded, leading to a sharp recovery in industrial metals and emerging market equities.

🥇 Precious Metals: The Clear Winner

Gold surged over 28% YTD, while silver gained around 25% — underpinned by a weakening dollar, central bank accumulation, and rising geopolitical risk.

Platinum emerged as the surprise outperformer, climbing over 30% YTD — widely seen as one of 2025’s “dark horse” assets.

🛠️ Industrial Metals: Fundamentals Regain Traction

Copper rose 23%, driven by structural demand from AI infrastructure, renewable energy build-outs, and electric vehicle supply chains.