AI Infrastructure Financing Fears Return to the Forefront

Bridging Structural Shifts Across Markets, Credit, and Technology

Executive Summary

Macro & geopolitics: Global markets remain shaped by persistent geopolitical risk, uneven disinflation, and diverging policy paths across major economies. These forces continue to channel capital toward structural, policy-backed themes, rather than short-cycle beta.

Structural theme in focus: AI-driven data-centre expansion is creating a multi-trillion-dollar financing requirement, with credit markets—particularly private credit and securitisation—emerging as the key transmission channel.

What’s next: We conclude with new trade ideas aligned with late-cycle AI infrastructure, capital bottlenecks, and mispriced financing beneficiaries.

Global Landscape: Policy, Geopolitics, and Capital Flows

Markets are becoming increasingly bifurcated. While headline inflation has moderated across developed economies, underlying structural pressures—energy security, defence spending, AI capex, and grid constraints—are intensifying.

As a result, fiscal policy and balance-sheet capacity, rather than marginal rate cuts alone, are becoming the dominant drivers of returns.

Europe has quietly entered a new phase of strategic rearmament.

The United States remains the global anchor for AI investment.

China is selectively easing policy to stabilise growth, creating pockets of opportunity amid still-cautious sentiment.

Deep Dive: The AI Data-Centre Financing Gap

AI is no longer a software story — it is a balance-sheet story.

Institutional research suggests global data-centre investment could reach ~USD 2.9 trillion through 2028, leaving an estimated USD 1.5 trillion external financing gap once hyperscaler cash flows are accounted for.

Key implications

Private credit is positioned to absorb the largest share, particularly via asset-based and project-level finance.

Securitised credit (ABS / CMBS) linked to data centres is emerging as a scalable, lower-cost funding channel.

Corporate bond issuance will rise more gradually, constrained by management reluctance to over-lever balance sheets early in the cycle.

This is not a speculative bubble dynamic. It is a capital-structure evolution, reminiscent of prior infrastructure build-outs—but with far higher asset quality, contracted demand, and visibility of cash flows.

Why This Matters for Investors

The market is still mispricing who truly benefits from this cycle.

The winners are not limited to chipmakers and hyperscalers, but also include:

Alternative asset managers scaling private credit

Banks and platforms facilitating structured finance

Infrastructure-linked equities exposed to power, cooling, and grid upgrades

Select credit instruments offering equity-like returns with contractual cash flows

In this phase, return on capital and balance-sheet durability, not revenue growth alone, will define outcomes.

‘Core–Satellite’ Positioning Framework

Our allocation framework follows a core–satellite structure, balancing durability with optionality.

The core focuses on scaled, cash-generative enablers of AI and data-centre expansion.

The satellite layer consists of higher-beta names that offer asymmetric upside as the AI infrastructure cycle broadens.

Core Holdings: Power, Grid, and Thermal Bottlenecks

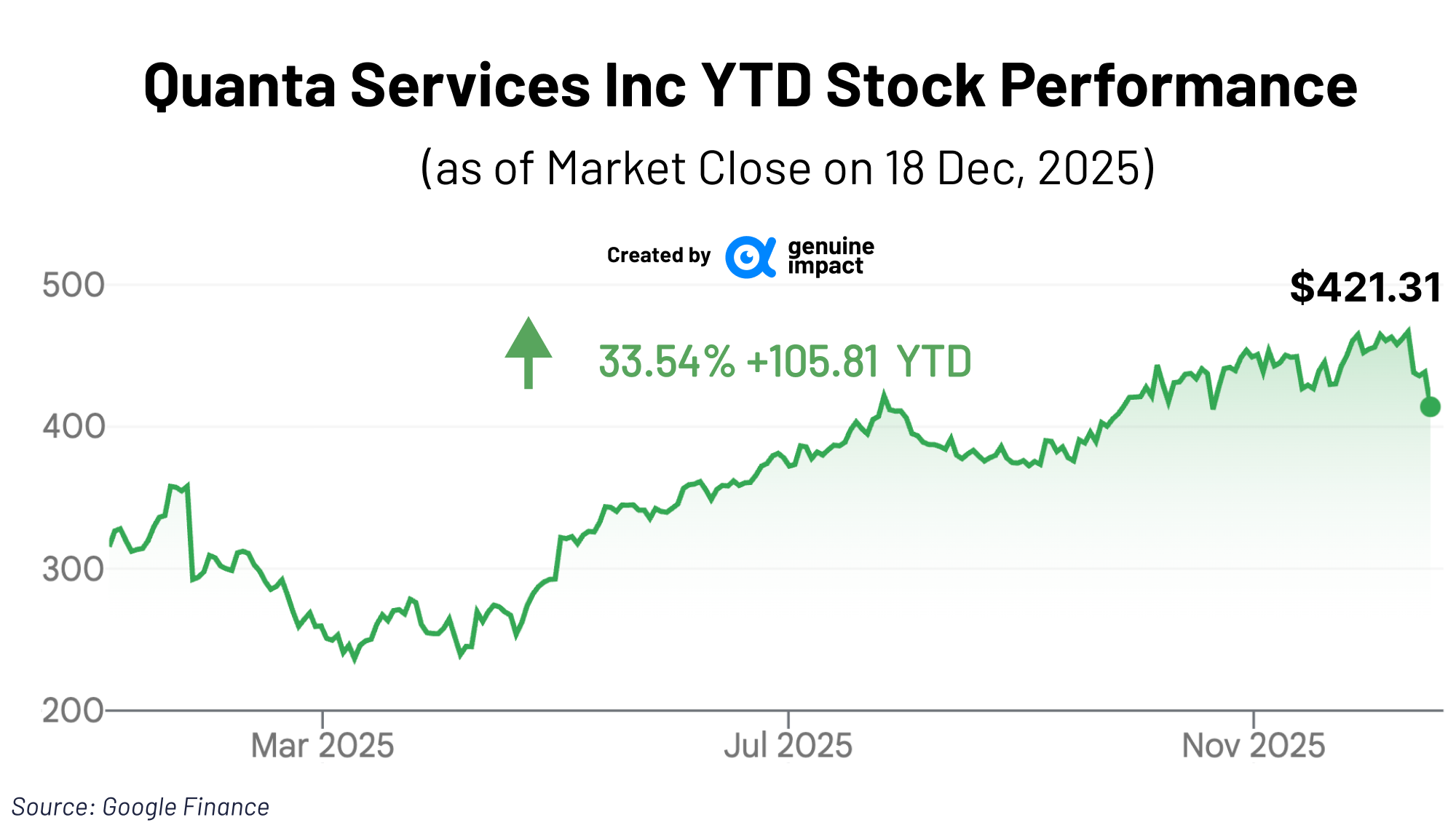

Quanta Services (+2.5% Core Portfolio Position)

Quanta Services sits at the critical junction between AI demand and physical power constraints.

As AI-driven compute growth collides with ageing grids, transmission bottlenecks, and permitting delays, Quanta is a key beneficiary of:

Grid modernisation

High-voltage transmission build-outs

Data-centre power interconnects and substation upgrades

Recent share-price weakness (–5.5% on Wednesday, 17 December) reflects broader market risk-off, not a deterioration in fundamentals.

In our view, Quanta represents a structural compounder in a world where AI growth is increasingly constrained not by GPUs, but by power availability.

Vertiv (+2.5% Core Portfolio Position)

Vertiv is a direct beneficiary of hyperscaler capex expansion, with exposure to:

Cooling systems

Power management

Thermal infrastructure

Rack-level densification

Two defining features of the AI era—higher power intensity per rack and thermal complexity—play directly into Vertiv’s operating leverage.

Importantly, recent volatility in AI infrastructure names has been driven not by demand concerns, but by renewed fears over financing.

This week, markets reacted sharply after reports that Blue Owl Capital exited financing talks for Oracle’s USD 10bn Michigan data-centre project, raising broader questions about who funds the next wave of GPU-intensive build-outs.

MarketWatch described the move as part of a broader AI-stock sell-off, rooted in concerns that data-centre expansion is becoming increasingly debt-dependent, while Barron’s highlighted investor sensitivity to financing risk following the Oracle news.

In this context, Vertiv’s role as a critical supplier, rather than a capital-intensive owner, positions it favourably in a tightening financing environment.

Satellite Watchlist: AI & Data-Centre Infrastructure Optionality

Alongside core holdings, we maintain a watchlist of satellite names — companies transitioning from crypto mining or digital platforms toward AI, HPC, and data-centre infrastructure.

These are not blanket recommendations, but monitored opportunities where execution milestones could materially re-rate valuations.

CleanSpark: Optionality tied to AI/HPC leasing at power-secured sites in Georgia and Texas.

Bitfarms: Repositioning toward AI/HPC in low-cost, cooler regions such as Quebec and Pennsylvania.

Soluna Holdings: Green data centres co-located with renewables, with a pipeline exceeding 1 GW.

Core Scientific: Advanced transition toward AI hosting, backed by ~1.3 GW footprint, but execution-sensitive.

Rumble: Aggressive pivot into AI cloud via the planned acquisition of Northern Data AG, with integration risk remaining key.

Portfolio Implementation: What We Are Adding

While satellite names remain under active review, our portfolio implementation is focused on scaling exposure within the core layer of the AI and data-centre ecosystem.

We plan to increase positions in infrastructure-critical names where:

Earnings visibility is higher

Balance sheets are stronger

Exposure is to enabling infrastructure, not financing risk itself

This reflects our broader conviction that the next phase of the AI cycle will be driven less by experimentation — and more by power, cooling, grid capacity, and execution discipline.

This information is for guidance purposes and may become out of date at any given time. It is not investment advice. Investments can rise and fall in value. Genuine Impact won’t make any assessment of whether the investments you choose are appropriate or suitable for you. If you are unsure of the suitability of any investment, investment service or strategy, you should seek independent financial advice. Past performance does not indicate future results. Your capital is at risk.

Love what you’re reading? Share this newsletter with your network and help them stay ahead of market trends. 💼📈

Keep in touch with Genuine Impact!

Instagram | X/Twitter | LinkedIn

Created by Arya & David