How Shopify Quietly Became a Global Checkout Powerhouse

Not Just a Website Builder

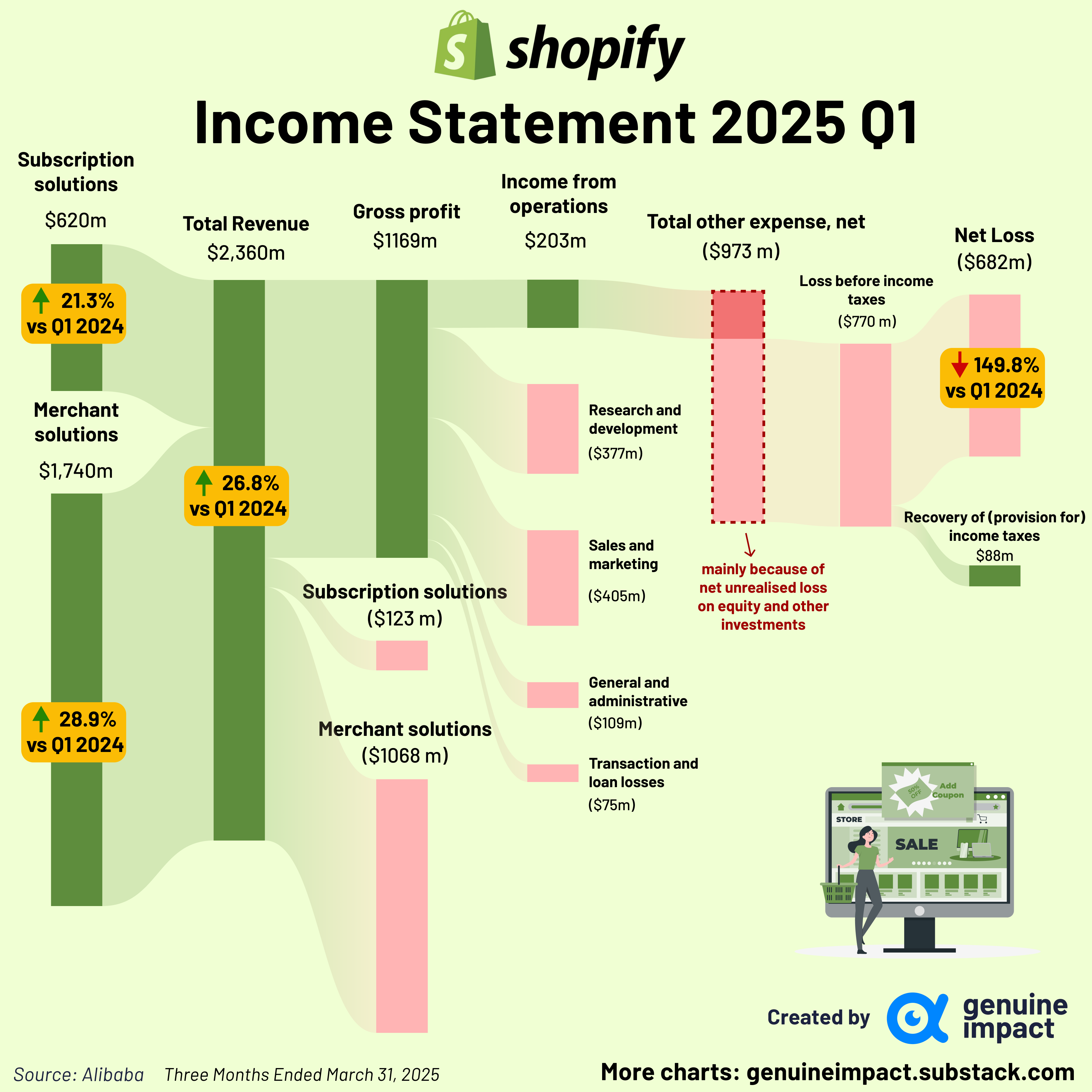

Shopify impressed with strong growth and profits.

Alibaba posted a huge profit jump, though modest revenue growth tempers the celebration.

Shopify: From Snowboards to SaaS Supremacy

What started as a side project to sell snowboards online has now become one of the world’s most influential e-commerce infrastructure providers. Welcome to the Shopify era—where scale meets simplicity, and margins now matter.

🚀 Growth That’s Built, Not Borrowed

Founded in 2006 in Ottawa, Shopify Inc. (NYSE/TSX: SHOP) has quietly redefined digital retail for everyone—from bedroom startups to brands like Gymshark and Heinz. Initially a scrappy Canadian underdog, the company now operates with dual headquarters in Ottawa and New York, a nod to its growing U.S. influence.

Shopify’s model is simple, but effective: give merchants the digital plumbing they need to sell anything, anywhere—then make money as they grow.

📈 Q1 2025 Results: Cash Flow and Confidence

Shopify delivered a Q1 2025 that beats expectations across the board:

Revenue: $2.36 billion (+27% YoY)

Free Cash Flow Margin: 15%

Gross Merchandise Volume (GMV): $74.75 billion

Monthly Recurring Revenue (MRR): $182 million

Operating Income: $203 million (more than doubled YoY)

Notably, this marks eight straight quarters of 25%+ revenue growth, and seven consecutive quarters of 20%+ GMV expansion.

And while geopolitical noise lingers—particularly Canada–U.S. trade tension—Shopify’s business remains impressively insulated, with no notable disruption reported to date.

Shopify recorded $1021 million in unrealised losses this quarter due to a decline in the fair value of its equity investments, including stakes in Flexport and others. These are non-cash accounting losses that do not impact the company’s actual cash flow, but are reflected in GAAP net income—resulting in an overall net loss for the quarter.

🧠 Strategy Shift: From Fulfilment Frenzy to Focused Core

2023 saw Shopify sell most of its logistics assets to Flexport, marking a pivot back to light-asset operations. Now, the company is leaning into high-margin segments:

AI-driven personalisation

The expanding Shop App

And scaling Shopify Plus, its enterprise-grade offering

Meanwhile, its Shopify Payments unit continues to gain ground in global checkout share. As of January 2025, Shopify holds 14.87% of the global online payment processing market—third behind only PayPal (45%) and Stripe (17%).

That’s not bad for a “website builder.”

💡 Why It Matters

Shopify is now more than a software company—it’s a full-stack commerce engine. With revenue increasingly driven by merchant solutions (payments, subscriptions, apps), it benefits not just from merchants joining the platform, but thriving on it.

Its strength lies in ecosystem stickiness:

Subscription revenue ensures stability

Payments and services scale with GMV

A thriving app marketplace deepens merchant reliance

From Ottawa origin story to global commerce backbone, Shopify’s evolution is far from over. With consistent growth, improving margins, and a focused strategy, it’s proving that SaaS can be both scalable and sustainable—even in a post-pandemic world.

Stay tuned for our Friday premium edition where we’ll break down portfolio moves, sector rotations, and our next trade idea — all for just $6/month (or £5/month).

Join 36,000+ savvy investors who believe: “Your money deserves better.”

In Case You Missed It 📬

Company Spotlight: Alibaba Group (NYSE: BABA)

Headquartered in Hangzhou, China, Alibaba Group Holding Limited released its financial results for the quarter and fiscal year ended 31 March 2025.

Q1 2025 Highlights (USD terms):

Revenue reached $32.58 billion, up 7% YoY.

Operating profit surged 93% YoY to $3.92 billion, driven by increased Adjusted EBITA and lower share-based compensation expenses.

Adjusted EBITA (non-GAAP) rose 36% to $4.50 billion, supported by revenue growth and improved operational efficiency, partially offset by continued investment in e-commerce and technology.

Net income attributable to shareholders came in at $1.71 billion.

Total net income jumped to $1.65 billion—up 1203% YoY—largely due to market gains in equity investments, stronger core earnings, and fewer impairments under the equity method.

This robust performance reflects Alibaba’s continued focus on streamlining operations while investing in long-term growth across its commerce and cloud segments.

Keep in touch with Genuine Impact!

Instagram | X/Twitter | LinkedIn

Created by Arya