Nvidia Just Reported the Greatest Quarter in Semiconductor History. The Stock Barely Moved.

$81.6 billion in revenue. $58.3 billion in net income. $91 billion guided for next quarter. And Nvidia closed down 1% after hours. What the market’s muted reaction tells us about AI investing.

On Wednesday evening, Nvidia reported the most extraordinary quarterly result in the history of the semiconductor industry.

Revenue of $81.6 billion. Net income of $58.3 billion — up 211% year-on-year. Data centre revenue of $75.2 billion, almost double what it was twelve months ago. Q2 guidance of $91 billion, clearing even the most aggressive whisper numbers on Wall Street. A new $80 billion share buyback. A 25-fold increase in the quarterly dividend, from 1 cent to 25 cents per share.

By any conventional measure, this was not just a good quarter. It was a historically unprecedented one. No semiconductor company has ever generated this level of revenue, this level of profit, or this level of forward visibility in a single reporting period.

Nvidia stock fell roughly 1% in after-hours trading.

That reaction — or rather, that absence of reaction — is the real story of the week. Not the numbers themselves, which were everything the bulls had hoped for, but the market’s increasingly sophisticated and unsentimental response to them. Understanding what happened on Wednesday night is understanding something important about where the AI trade is right now.

“The buildout of AI factories — the largest infrastructure expansion in human history — is accelerating at extraordinary speed. Agentic AI has arrived. Compute capacity is profits.” — Jensen Huang, Nvidia CEO, May 20 2026

I. The Scorecard

The numbers reported on Wednesday evening deserved more celebration than they received. Here is what Nvidia actually delivered:

Revenue (Q1 FY2027) $81.6bn vs $78.8bn consensus — beat by $2.8bn

Year-on-year growth +85% vs +77% expected

Sequential growth +20% quarter-on-quarter

Data Centre revenue $75.2bn vs $73.1bn consensus — up 92% YoY

Non-GAAP EPS $1.87 vs $1.77 consensus — beat by 6%

Gross margin 74.9% held firm, in line with guidance

Net income $58.3bn up 211% year-on-year

Free cash flow $48.6bn record quarterly FCF

Q2 FY2027 guidance $91bn vs $86.8bn consensus — beat by $4.2bn

Share buyback authorised $80bn new programme

Quarterly dividend $0.25/share 25x increase from prior $0.01

Every single line item beat. The forward guidance cleared even the most aggressive buy-side whisper numbers. The margin held. The free cash flow was a record. And Jensen Huang unveiled the next generation of Nvidia’s architecture — the Vera CPU and Rubin GPU systems — extending the product roadmap that has underpinned the AI infrastructure buildout.

For context: Nvidia generated more net income in a single quarter — $58.3 billion — than the entire annual revenues of most FTSE 100 companies. It generated more free cash flow in 90 days than the GDP of many sovereign nations. This is a company operating at a scale that has no precedent in the technology industry.

II. Why the Stock Barely Moved

Nvidia has now beaten Wall Street’s earnings estimates in 18 of the last 20 quarters. It beat in every single quarter of the AI cycle. And in each of the three most recent reporting periods, the stock has fallen on the day of the results despite the beat — three consecutive earnings-day declines on three consecutive beats.

This pattern is not irrational. It is the natural consequence of a stock that has already priced in excellence. When a company is expected to deliver extraordinary results with 97% probability, extraordinary results are not news. They are confirmation of the existing thesis. The market does not re-rate a stock for doing what it was already expected to do.

The last time Nvidia produced a double-digit stock move in response to earnings was more than two years ago, in early 2024. At that point, the AI trade was still early-stage and the magnitude of the demand was genuinely surprising. In May 2026, with $725 billion in hyperscaler AI capex already on the books and Nvidia’s dominance well-established, the surprise element has been substantially compressed.

The three questions the market is sitting with:

Beyond the priced-in excellence dynamic, three specific concerns are keeping a ceiling on Nvidia’s re-rating despite the extraordinary results.

First, China. Nvidia’s guidance explicitly excludes any data centre compute revenue from China. Jensen Huang joined Trump’s Beijing delegation on May 14 — Trump personally added him to the list — and the US has cleared around 10 Chinese firms including Lenovo to buy H200 chips. But not a single delivery has been made. Chinese companies pulled back after guidance from Beijing, even after Washington gave the green light. Huang estimates China’s AI chip market at approximately $50 billion annually. That number is currently zero on Nvidia’s books. Every quarter it stays there is a quarter where the most obvious upside optionality goes unrealised.

Second, the custom silicon threat. As we covered in last week’s edition, Google’s TPU programme, Amazon’s Trainium, and Meta’s MTIA are all scaling. The hyperscalers committing $725 billion in combined AI capex are simultaneously Nvidia’s best customers and its most credible competitors. The Q2 guidance of $91 billion is strong enough to suggest this threat is not yet impacting Nvidia’s near-term revenues. But the market is forward-looking, and a future in which a meaningful share of hyperscaler compute runs on in-house silicon is already being partially priced.

Third, the architecture transition risk. Nvidia is currently mid-transition from Blackwell to Vera Rubin. Blackwell shipments are winding down; Rubin production is accelerating. Transitions of this kind have historically created air pockets in revenue as the old product cycle closes and the new one ramps. Huang’s language on the call was confident, but supply chain constraints on Rubin availability through the second half of 2026 remain a live concern.

The bull case requires Jensen Huang to do what he has done every single quarter of this cycle: deliver, and then raise. He did exactly that on Wednesday. The stock’s muted reaction says less about Nvidia than it does about the market’s relationship with certainty.

III. The Number That Actually Matters: $91 Billion

While the Q1 results were the headline, the most important number in Wednesday’s report was the Q2 guidance: $91 billion in revenue, plus or minus 2%.

This matters for three reasons. First, it cleared the whisper number. Buy-side desks were running internal models at $88-90 billion. At $91 billion, Nvidia not only beat the published consensus of $86.8 billion — it beat the informal bar that sophisticated investors had set privately. That is the threshold that, in previous quarters, has produced the strongest stock reactions.

Second, $91 billion in a single quarter annualises to $364 billion in annual revenue. Huang himself has guided to $1 trillion in revenue from Blackwell and Rubin across 2026 and 2027. If Q2 comes in at or above $91 billion, the path to that $1 trillion figure becomes mechanically clearer, not just aspirational.

Third, the $91 billion guidance was issued with no China revenue assumed. If the diplomatic groundwork laid in Beijing begins to translate into actual chip deliveries — even partially, even at discounted prices to account for the 25% US government revenue share — there is a material upside scenario that is not in the current numbers. Huang estimates that market at $50 billion per year. Any fraction of it flowing back into Nvidia’s guidance would be a significant positive revision.

The sovereign AI dimension adds another layer. This is the revenue stream — national governments building domestic AI infrastructure using Nvidia chips — that has received far less attention than the hyperscaler story. According to prior management guidance, sovereign AI revenue crossed $30 billion in fiscal 2026, more than tripling year-on-year and accounting for approximately 14% of total revenue. Customers include the UK, France, the Netherlands, Singapore, Canada, and India, which announced a $1 billion sovereign AI programme with Nvidia. This is a demand channel driven by geopolitical strategy rather than commercial return calculations, which makes it structurally stickier and less sensitive to valuation concerns about AI ROI.

IV. The Broader Market Context

Nvidia’s results do not exist in isolation. They landed in a week that was, outside the Nvidia story, deeply uncomfortable for markets.

Bond markets revolt:

UK Gilt yields hit levels not seen since 1998 this week — the 30-year Gilt touched 5.747%, its highest since March 1998. The US 10-year Treasury yield reached 4.67%, its highest in over 15 months. The 30-year US Treasury briefly hit 5.197%, its highest since 2007. The market is now pricing a 28% probability of a Federal Reserve rate hike at its December meeting — a number that was essentially zero six weeks ago. April CPI came in at 3.8% year-on-year, the hottest reading since May 2023, driven primarily by elevated oil and gasoline prices from the Strait of Hormuz disruption.

The S&P 500 fell for three consecutive days earlier in the week, its longest losing streak since March, before recovering somewhat on Wednesday as markets positioned ahead of Nvidia’s results. The equal-weight S&P 500 outperformed the cap-weighted index on Monday — a technical signal that the mega-cap AI names that have been carrying the index are beginning to see rotation out, even as their earnings remain exceptional.

The yield curve signal:

The divergence between what bond markets and equity markets are pricing is now at its most acute since before the Iran conflict began. Equities are at record highs, pricing continued AI-driven earnings growth and an eventual Fed pivot. Bond markets are pricing persistent inflation, no cuts in 2026, and a non-trivial probability of a hike. One of them is wrong. Historically, when that divergence has resolved, it has been equities that have adjusted to bond market reality rather than the reverse.

For Nvidia specifically, the yield environment matters. The company’s valuation — even at a relatively reasonable 47 times trailing earnings given its growth rate — is sensitive to the discount rate applied to future cash flows. If real yields stay elevated or rise further, the multiple compression risk remains live even as the earnings trajectory continues upward.

Iran: pause but not resolution

Trump called off a planned resumption of military strikes on Iran on Tuesday, citing “serious negotiations” toward a peace deal. Oil fell on the news, providing some relief. But the Strait of Hormuz remains effectively closed, Brent crude is still above $95, and the structural inflation pressure from energy has not resolved. The ceasefire dynamic is the single most important macro variable for the rate outlook — and therefore for gold, bonds, and indirectly for high-multiple growth stocks like Nvidia.

V. What This Means for Investors

The week’s events crystallise three actionable observations for investors navigating this environment.

On Nvidia specifically:

The results validated the structural thesis entirely. Revenue growth of 85%, data centre revenue nearly doubling, $91 billion guided for next quarter — these are not the numbers of a company whose competitive moat is eroding. The China optionality ($50 billion annually, currently zero in the guidance) and the sovereign AI ramp (crossed $30 billion in fiscal 2026 per prior management guidance, roughly 14% of revenue) are two underappreciated upside levers that are not yet fully visible in consensus models.

The muted stock reaction is less a verdict on Nvidia’s business and more a function of positioning. The stock rallied 40% from its March lows into the print. At a $5.7 trillion market cap, moving the needle requires not just a beat but a beat of sufficient magnitude to justify further re-rating. Wednesday’s results were excellent. They were not, in the context of what was already priced, a surprise.

Bank of America’s price target of $320 implies approximately 40% upside from current levels. The analyst consensus sits at $272-279 — roughly 21-24% upside. The Computex trade show in early June and the Vera Rubin architecture launch in the second half of 2026 are the next catalysts in the sequence.

On the AI trade more broadly:

The AI buildout is not slowing. $725 billion in hyperscaler capex, $91 billion in Nvidia’s next quarter guidance, Google’s TPU programme scaling to external customers, sovereign governments committing billions to domestic AI infrastructure — these are not the characteristics of a trade that is running out of fuel. They are the characteristics of a trade that is maturing from its speculative phase into its infrastructure phase.

The infrastructure phase of a technology cycle tends to reward different assets than the speculative phase. In the speculative phase, the primary beneficiary is the company that captures the excitement — Nvidia itself. In the infrastructure phase, the rewards begin to spread: the energy suppliers powering the data centres, the real estate investment trusts owning the facilities, the networking companies connecting the compute, the software layers monetising the inference. Keel Infrastructure’s 22% week two weeks ago was a signal of this broadening.

On the macro environment:

The bond market’s message this week was clear: do not assume the inflation problem is solved, and do not assume the Fed will rescue equities with rate cuts. UK 30-year Gilt yields at their highest since 1998, the US 30-year Treasury at its highest since 2007, and a 28% probability of a December Fed hike are not background noise. They are the most important signal in the market right now — and they are pointing in the opposite direction to record equity highs.

The resolution of this divergence is the central question for markets through the summer. If Iran negotiations produce a genuine ceasefire and oil falls materially, the inflation picture improves, the bond market rally returns, and equities have room to extend their gains. If negotiations stall or break down, the energy shock deepens, inflation stays elevated, and the Fed’s hand is forced. Nvidia’s results are extraordinary either way. The question is what multiple the market awards those results in each scenario.

The Bigger Picture

There is a version of this week’s story that writes itself as straightforwardly bullish. Nvidia delivered the greatest quarter in semiconductor history. The AI buildout is accelerating. The sovereign AI market is growing. The China optionality has never been larger. Jensen Huang’s confidence is unshaken.

That version is not wrong. But it is incomplete.

The complete version includes a bond market pricing out rate cuts and pricing in hikes. UK 30-year Gilts at their highest since 1998. The US 30-year Treasury at its highest since 2007. US inflation at 3.8%. Oil above $95 despite a diplomatic pause. A stock that fell on what may be the best quarterly result its industry has ever produced.

What we are watching in real time is the collision between two genuine forces: an AI earnings cycle that is delivering on its extraordinary promise, and a macro environment that is making it progressively harder to award those earnings the multiples they deserve. Nvidia’s business has never been stronger. The context in which it operates has rarely been more complicated.

Compute capacity is profits, as Jensen Huang said on Wednesday night. The question the market is asking back is: at what discount rate?

That question will be answered not in Nvidia’s next earnings call but in the next CPI report, the next FOMC meeting, and the next development in the Strait of Hormuz. The AI story is intact. The macro story is the variable. And right now, the macro is the one doing the talking.

Insider Portfolio Performance

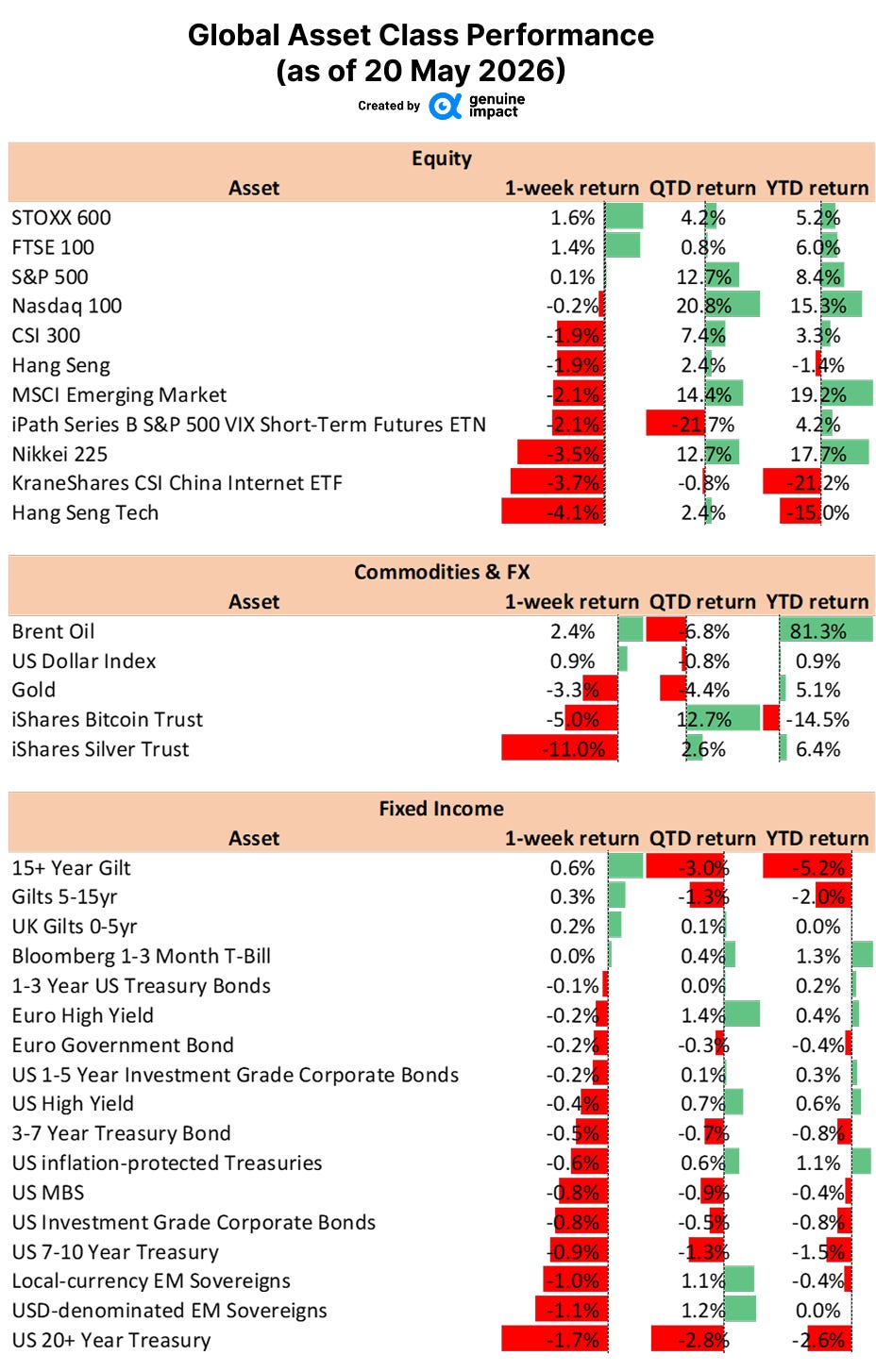

Global markets this week were mixed, with European equities showing relative strength while Asia, China tech, crypto, precious metals, and longer-duration fixed income came under pressure.

The STOXX 600 and FTSE 100 rose 1.6% and 1.4% respectively, while the S&P 500 was broadly flat and the Nasdaq 100 slipped slightly. The weakness was more visible in Asia and high-beta growth: MSCI Emerging Markets fell 2.1%, KWEB dropped 3.7%, and Hang Seng Tech declined 4.1%.

Commodities also showed a clear split. Brent Oil rose 2.4% and the US Dollar Index gained 0.9%, but gold fell 3.3%, bitcoin exposure declined 5.0%, and silver sold off sharply, down 11.0%. Fixed income offered limited protection, with most bond exposures negative on the week, especially longer-duration US Treasuries.

‼️ This week was a difficult one for the portfolio, with pressure concentrated in China tech, high-beta growth, crypto-linked exposure, and quantum computing names. However, selected AI software and defence positions helped offset some of the weakness.

Full performance details below ⬇️