🧠 Palantir: Deep Tech, Deeper Moats

But Is It Too Expensive to Touch?

Palantir extended its winning streak with a blowout Q1, but a sky-high valuation has investors asking: is the price of ambition too steep?

Amazon posted a solid quarter with AWS and retail firing on all cylinders—yet soft free cash flow hints at the cost of staying on top.

Palantir (NYSE: PLTR) just posted another strong quarter, sending ripples through the AI and defence tech investment landscape. Its results point to a company building not just software platforms, but strategic entrenchment across government and enterprise.

1. A Dual-Core Business Model 🔍

Palantir’s operations centre around two flagship platforms:

Gotham – Its original government-focused platform, Gotham is used by U.S. intelligence agencies, military forces, and law enforcement. It excels at integrating multi-source data into mission-critical insights for counterterrorism, battlefield decision-making, and surveillance. Its strengths lie in visualisation, target tracking, and link analysis—making it essential for national security operations.

Foundry – Built for commercial clients, Foundry powers predictive modelling, supply chain management, and operational optimisation. Global giants like Airbus, BP, and Pfizer use Foundry to bridge data silos and accelerate strategic decisions—no code required. Foundry’s “Ontology” layer maps business logic to AI workflows, enabling companies to embed automation into core processes.

AIP (Artificial Intelligence Platform) – Launched in 2023, AIP integrates large language models (like GPT) into secure private deployments. It’s already being used in defence simulations and enterprise decision-making—pushing Palantir to the frontier of AI-native architecture.

🔧 Not Just SaaS: Strategic Co-Building

Palantir operates a hybrid model—part subscription software, part embedded consultancy. It’s not just selling platforms; it’s helping clients rewire how decisions get made. This “strategic partner” approach leads to long-term contracts and deep operational integration. In other words, once Palantir is inside, it’s difficult to remove.

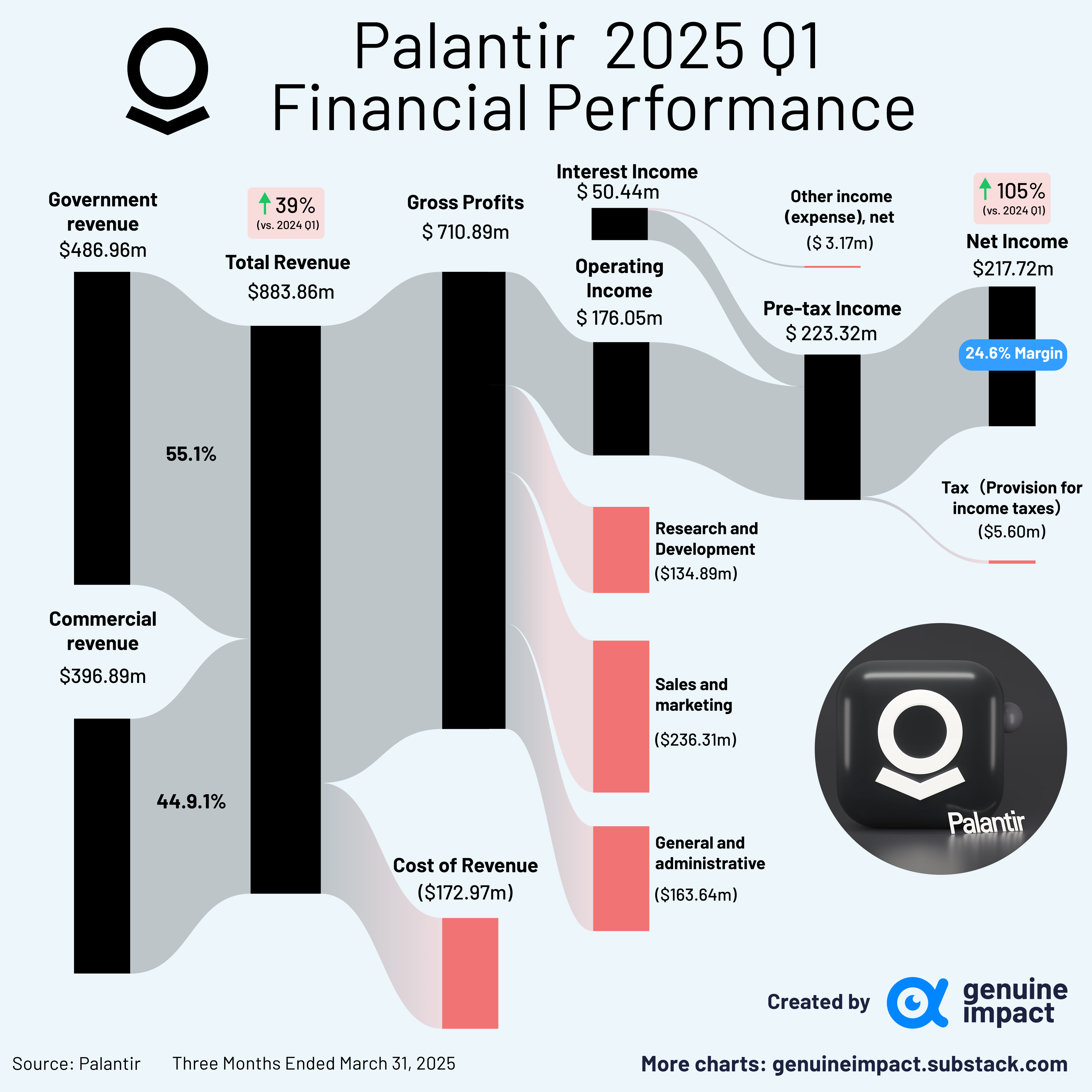

📈 2. Financial Highlights: Q1 2025

Palantir’s Q1 results paint a picture of momentum、

Total revenue: $884M (+39% YoY, +7% QoQ)

U.S. commercial revenue: $255M (+71% YoY)

U.S. government revenue: $373M (+45% YoY)

Free cash flow: $370M (42% margin)

Contract wins: 139 deals over $1M; 31 over $10M

Customer count: +39% YoY

Commercial TCV booked: $810M (+183% YoY)

The numbers signal scale and stickiness. Notably, U.S. commercial deal value surged, indicating that Palantir’s enterprise efforts are no longer in pilot—they’re production-grade.

3. Is It a Buy? The Valuation Debate 📉

Palantir’s shares have soared over 1,000% in the last three years, pushing its forward P/E ratio to over 200, reaching 623 on 12th May — a level that many investors would find hard to stomach.

Yes, it’s arguably one of the most commercially viable AI platforms out there today. Compared to speculative AI plays like IonQ, Palantir looks mature and grounded. But even bullish analysts are hesitant. The company is executing—but the market has priced in a near-flawless future.

As one strategist put it: “It’s a great business, but a difficult stock to buy at these levels.” We tend to agree.

📌 Bottom Line

Palantir’s Q1 results underscore its evolution from secretive contractor to commercial AI force. With strong fundamentals, expanding use cases, and rising cash flow, it checks every box—except valuation. For now, we’re watching closely, but waiting for a more reasonable entry point.

Stay tuned for our Friday premium edition where we’ll break down portfolio moves, sector rotations, and our next trade idea — all for just $6/month (or £5/month).

Join 36,000+ savvy investors who believe: “Your money deserves better.”

In Case You Missed It 📬

Amazon Delivers a Solid Q1

Amazon (AMZN) reported Q1 2025 net sales of $155.7B (+9% YoY), with net income surging 65% to $17.1B. EPS came in at $1.59, up from $0.98 a year ago.

🌍 Regional & Segment Highlights:

• AWS revenue: $29.3B (+17%)

• North America sales: $92.9B (+8%)

• International sales: $33.5B (+5%)

• Operating income: $18.4B (+20%)

💰 Operating cash flow rose to $113.9B, while free cash flow declined to $25.9B, reflecting continued investment.

Despite FX headwinds and macro uncertainty, Amazon’s cloud and retail momentum remains strong.

Keep in touch with Genuine Impact!

Instagram | X/Twitter | LinkedIn

Created by Arya