Tokenisation Solved Distribution, Not Liquidity

The tokenised real-world asset market is quoted at $345 billion, but far less trades. Tokenisation has worked as distribution for liquid assets, not as a solution to illiquidity.

Real-world asset (RWA) tokenisation is the issuance of a digital token on a blockchain that represents ownership or economic rights in a traditional asset, such as a Treasury bill, a private loan, or a bar of gold. The technology has moved from pilots to production, and the largest asset managers now run live products. This issue makes one argument: the first wave of tokenisation is a money-market story, not a market-transformation story. It has added efficient on-chain distribution to assets that were already standardised and liquid, while the assets that were supposed to be transformed, real estate and private credit, remain about as illiquid on-chain as off it. The sections below set out the framework for reading the market, explain why Treasuries won and the illiquid categories stalled, connect the regulation to the same question, and end with what it means for an allocator.

I. Four Numbers, Not One

The market is usually described with a single large figure. Reading it well takes four, arranged as a ladder that runs from what exists on a ledger down to what a holder can actually sell.

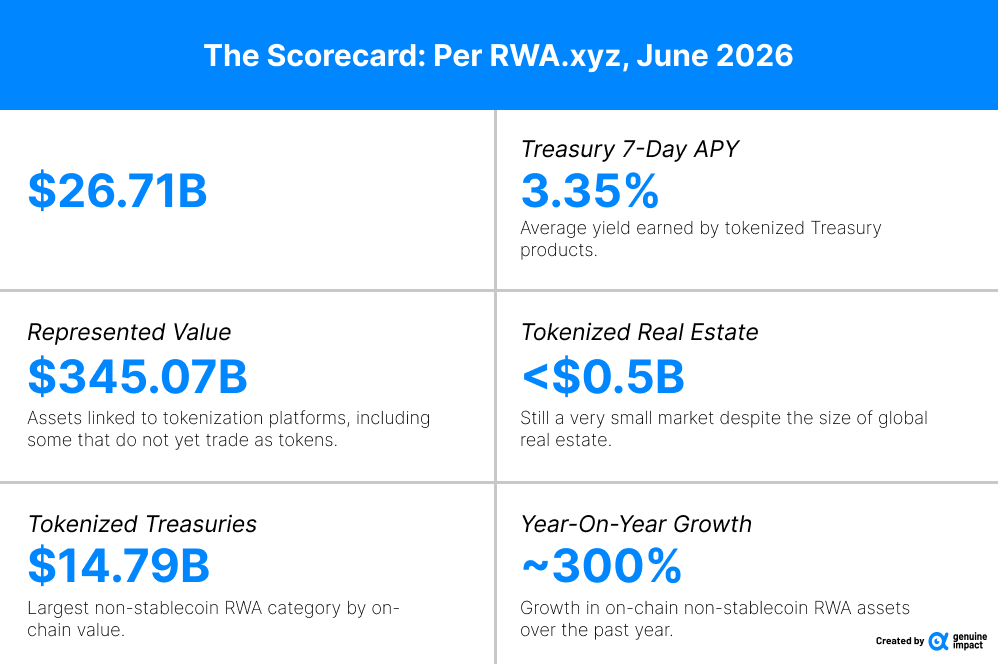

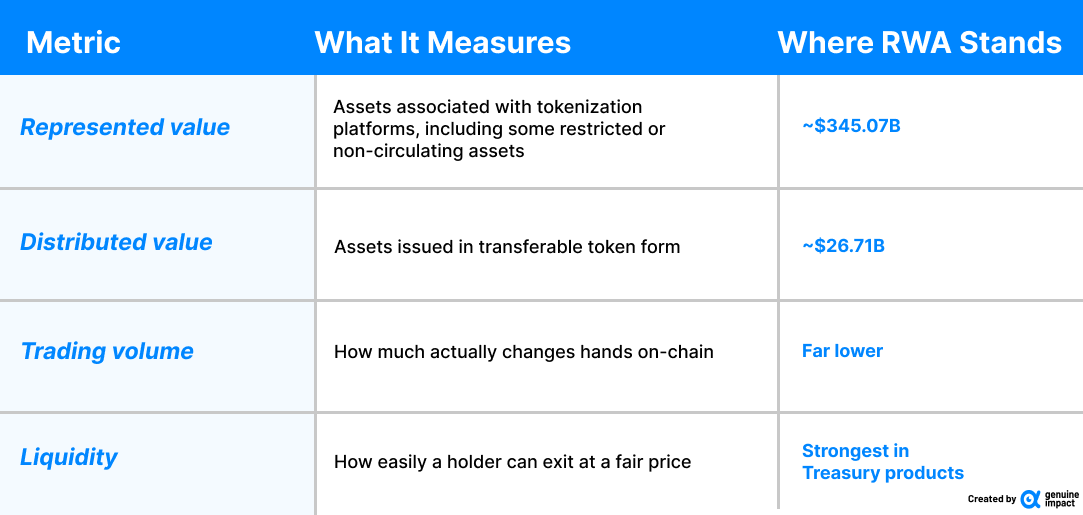

The two figures most coverage cites sit at the top of the ladder. Represented value, roughly $345.07 billion, counts assets represented on tokenisation platforms, not all of which circulate as transferable tokens; some are recorded on-chain as a system of record, such as loans, rather than issued as freely tradable tokens. Distributed value, roughly $26.71 billion across about 698,200 holders, is the amount actually issued as tokens that can circulate.

The important correction is below that. A token that is transferable is not the same as a token that is liquid. A position can be issued, legally tradable, and still almost never change hands. A 2026 study of on-chain RWA data found that most tokens show low trading volumes, long holding periods, and limited participation. So the real measure of the market is not the headline, and not even the distributed figure. It is how much trades, and how easily a holder can get out.

Transferable is not liquid. A token can be issued, legally tradable, and still never trade.

II. Why Treasuries Won

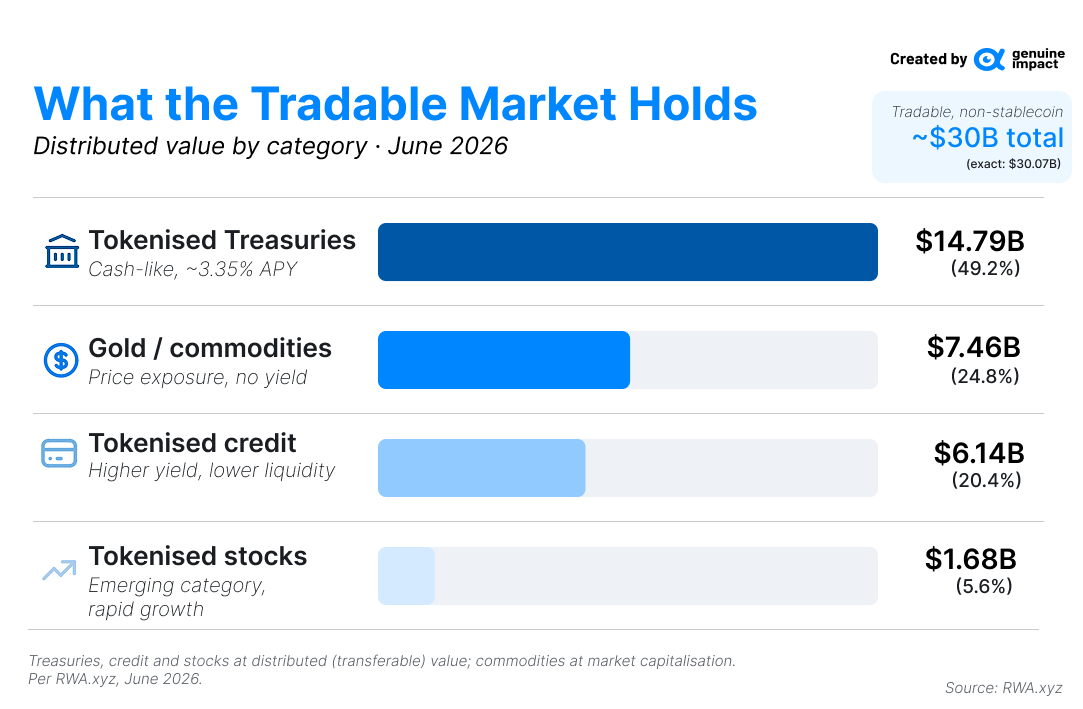

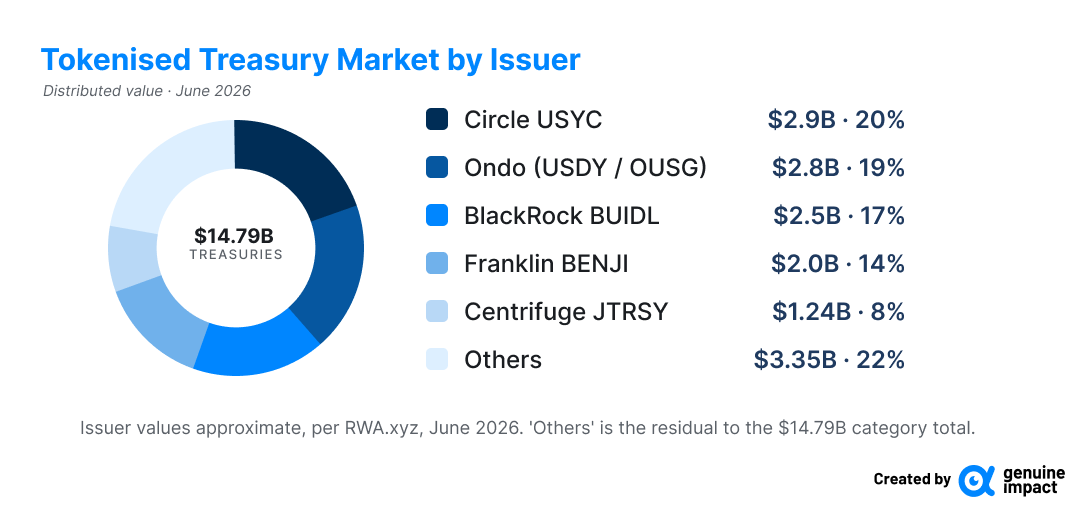

Almost half of all tokenised RWA value sits in US Treasuries, about $14.79 billion across 82 products, paying a 3.35% seven-day yield. That concentration is not an accident. Treasuries dominate because they already possess the three properties tokenisation needs to work: standardised ownership, continuous daily pricing, and institutional custody. A Treasury bill is identical to every other unit of the same series, it is priced every day in the deepest market in the world, and its custody is already handled by existing financial infrastructure.

Tokenisation does not transform that asset. It adds a round-the-clock settlement rail to something that was already liquid and fungible. This is the success case, and it is worth being precise about what kind of success it is. It is distribution, not transformation: a better pipe for moving an asset that already worked

The issuer market is tight and institutional. Circle's USYC holds about $2.9 billion, Ondo's suite about $2.8 billion, BlackRock's BUIDL about $2.5 billion, and Franklin Templeton's BENJI about $2.0 billion. BUIDL is the reference for how these are built: a $5 million minimum restricted to US qualified purchasers, with BNY Mellon as custodian and Securitize as transfer agent, deployed across eight chains, and the fastest tokenised fund on record to reach $1 billion. Even in the largest product, holders number in the double digits and the biggest transfers cluster near $10 million each. This is institutional plumbing, not a deep retail market, which is the point: the validated use case so far is moving cash-like instruments between large balance sheets.

III. Why the Illiquid Stayed Illiquid

The categories that were supposed to be transformed have barely moved. Tokenised real estate, once described as the technology’s flagship use case, remains in the low hundreds of millions of dollars, a rounding error against a multi-trillion global property market.

The reason is causal, not incidental. Real estate has not scaled because its frictions are legal and structural, and a token cannot resolve any of them: jurisdiction-specific property law, title registration, local tax treatment, and the enforcement of income rights. Tokenising a building records who owns a claim; it does not change what that claim is worth to sell, who is allowed to buy it, or how a dispute is settled. Fine art and other unique assets face the same problem in sharper form.

Private credit shows the same gap inside the numbers. Figure’s home-equity token records roughly $18.82 billion in represented value, while total tokenised credit distributed value is closer to $6.14 billion. The blockchain is acting as a system of record for loans that do not circulate as tokens. The deeper point sits one rung lower on the ladder: issuing a token for an illiquid asset does not summon a buyer on the other side of the trade. Outstanding value rises; turnover does not follow.

Interpretation: the headline yield on tokenised private credit, roughly 8 to 15%, is compensation for that illiquidity, not evidence that tokenisation has removed it. Tokenisation has digitised assets that were already liquid far more successfully than it has unlocked assets that are not.

A token for an illiquid asset records ownership. It does not create a buyer.

IV. Regulation Is the Gate to Liquidity

Regulation matters here only where it moves the ladder. The GENIUS Act, signed into law on 18 July 2025, set reserve and monthly disclosure rules for payment stablecoins, which are the settlement leg for most tokenised trades. Its effect is to harden the rails under the liquid layer, the cash-like products that already work.

The harder question is securities, and that is where liquidity for the stalled categories will be decided. The Digital Asset Market Clarity Act would set the broader market structure. It passed the House in 2025, the Senate Banking Committee advanced its version by 15 to 9 on 14 May 2026, and it reached the Senate legislative calendar on 1 June 2026, still short of a full-Senate vote. In March 2026 the SEC stated that a security is treated as a security whether it is issued on-chain or off-chain.

This connects directly to the thesis. A genuine secondary market for a tokenised equity or fund interest cannot form until the token’s legal status is settled, specifically whether the token is the registered security itself or merely a claim referencing one. That distinction governs who can hold it, how it clears, and whether it can be sold freely. Regulation is therefore the precondition for liquidity in exactly the categories that lack it. For Treasuries, the rules are already clear and the market already works. For everything harder, the law is the bottleneck.

V. What This Means for Investors

The framework above points to different conclusions for each category. These are reads of the current data rather than recommendations, and they distinguish what is established from what is still speculative.

Tokenised Treasuries are the validated category.

Real government yield around 3.35%, daily redemption, and institutional custody. The use case is operational efficiency, not speculation. The main risk sits in the token layer itself, smart-contract, custody, and bridge risk, rather than in the underlying bill.

Private credit is high-yield but not liquid.

Yields of roughly 8 to 15% compensate for a genuine lock-up. A tokenised credit position is best treated as held to maturity, not as something that can be exited on demand, regardless of the wrapper around it.

Tokenised equities are the most plausible next growth area, and the most regulation-dependent.

The value turns entirely on whether the token is the registered share or a synthetic claim, which determines voting, dividends, and the right to exit. Watch the CLARITY Act and SEC rulemaking, not the AUM headlines.

Real estate and other illiquid assets remain early.

Tokenisation has not changed the underlying illiquidity, so headline AUM in these categories says little about whether a position can be sold.

The metric to track is secondary-market turnover, not assets under management.

AUM measures issuance. Turnover measures whether a market exists. For now, the two diverge sharply outside Treasuries.

VI. What To Watch

Signals for the next quarter

Secondary-market turnover. Whether trading volume starts to rise in private credit and real estate, the test of whether tokenisation is moving from distribution to liquidity.

The CLARITY Act timeline. Whether the Senate finds floor time before the summer recess, and how the final text defines a tokenised security.

Represented-to-distributed conversion. Whether platforms mint more of the $345 billion into transferable form, which would narrow the gap between headline and reality.

New asset classes from institutions. Morgan Stanley’s planned tokenised-equity trading and JPMorgan’s stablecoin-issuer Treasury fund, both of which would extend the validated layer.

VII. The Read

The first wave of tokenisation is a money-market wave. It has proven, at production scale and with the largest managers behind it, that a liquid and standardised asset can be distributed efficiently on-chain. That is a real achievement, and it is the reason Treasuries make up almost half the market. The open question, and the one that decides whether the $16 trillion projections mean anything, is whether tokenisation can create liquidity where none exists rather than just digitising liquidity that already did. Until secondary volumes rise in the illiquid categories, the honest description of the market is narrow and institutional: a new distribution layer for liquid assets, rather than a solution to illiquidity itself.

Insider Portfolio Performance

🚨 Major Update: Genuine Impact Insider Portfolio Is Now Genuine Impact AI Portfolio

We’re excited to announce that the Genuine Impact Insider Portfolio has officially been upgraded to the Genuine Impact AI Portfolio. 🚀

This marks an important evolution in our investment framework: moving from a broader global equity approach toward a more focused strategy built around one of the most powerful structural growth themes of this decade: artificial intelligence. 🤖

AI is reshaping corporate investment, productivity, and the global technology value chain. The new Genuine Impact AI Portfolio is designed to capture this opportunity across the full AI value chain, with exposure to key areas such as compute infrastructure, agentic AI, physical AI, and the physical infrastructure required to support the data-centre build-out. 🌐

In short, this upgrade reflects a shift from simply participating in the AI trend to actively positioning around the companies enabling, scaling, and monetising the AI revolution. 📈

‼️ The AI Portfolio gave back ground this week, caught in the broad risk-off move across technology. Most of the book fell with the market, though a handful of positions stayed positive and softened the decline. The year-to-date gains held.

How the AI Portfolio navigated the sell-off, with full holdings and performance, below ⬇️