🧭 Your Weekly Market Decode

Fed succession signals, BoJ turns hawkish, and precious metals surge

Executive Summary

Markets traded calmly despite a heavy flow of macro signals.

President Trump confirmed he has already chosen the next Fed Chair, reinforcing expectations that the nominee will support rate cuts in 2026.

In the UK, the Autumn Budget surprised positively for gilts, while in Japan, BoJ Governor Ueda indicated the central bank is prepared to raise rates at the 18–19 December meeting, lifting market-implied hike probabilities to 75–80%.

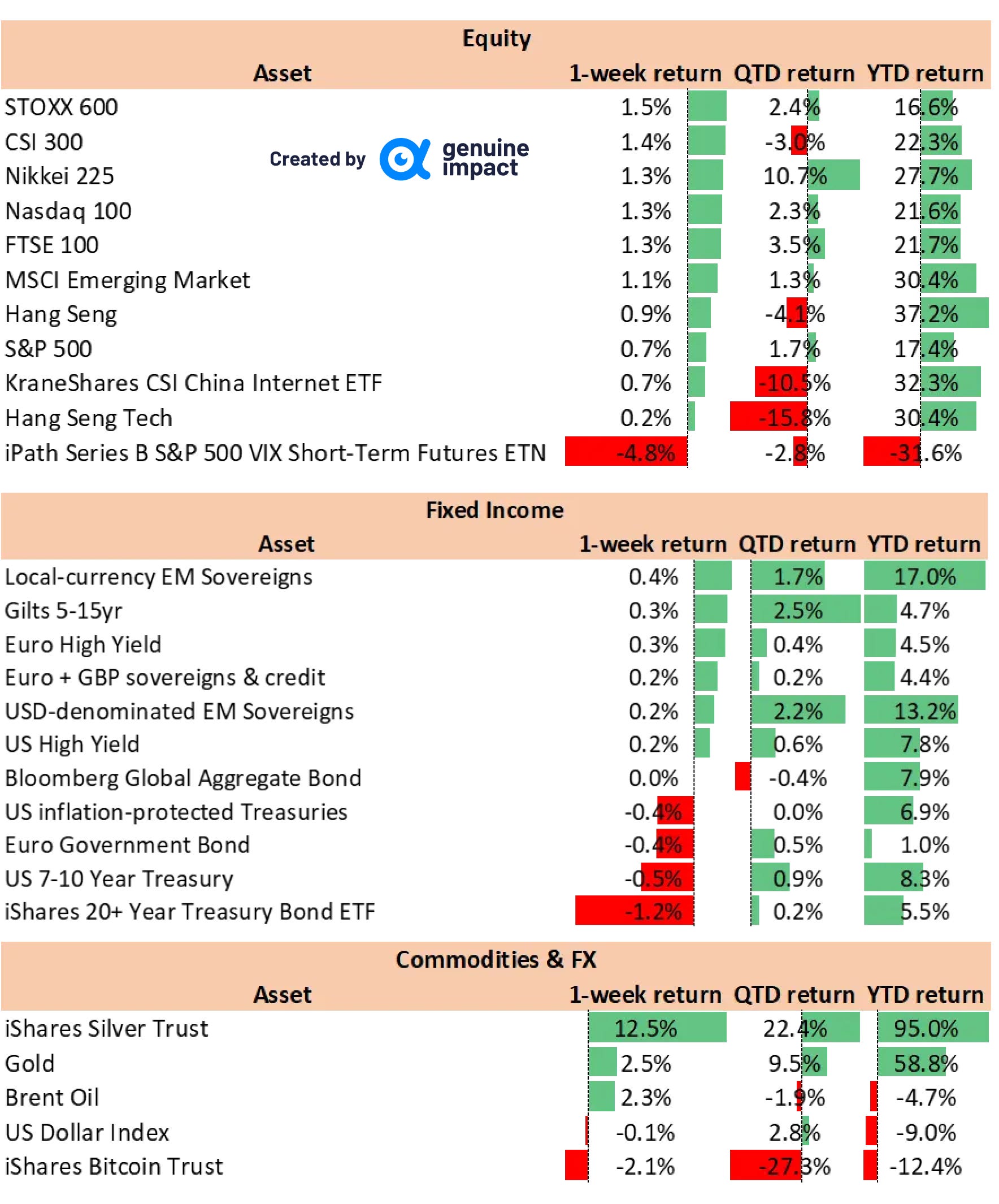

Across commodities, precious metals extended their rally — gold +2.5%, silver +12.5% — supported by expectations of Fed easing and tightening supply dynamics in China.

1️⃣ Global Market Review

🇺🇸 United States

Markets focused on Fed succession signalling as President Trump stated he has “already decided” on the next Federal Reserve Chair, adding that he expects the nominee to push forward with rate cuts.

Informal chatter suggests an announcement around Christmas.

Soft manufacturing data added to the picture:

ISM Manufacturing PMI fell to 48.2 in November (vs 48.7 in September), the weakest reading in four months and below consensus expectations of 48.6.

The data reinforces the narrative of slow but controlled cooling in the US industrial cycle.

🇪🇺 Euro Area & 🇬🇧 United Kingdom

Euro Area Inflation:

November CPI accelerated slightly to 2.2% YoY (vs 2.1% prior), above expectations.

Services inflation: 3.5% (highest since April)

Energy inflation: –0.5% (vs –0.9% prior)

The profile remains sticky, delaying expectations for a decisive ECB pivot.

Germany:

GfK Consumer Climate improved to –23.2 (from –24.1), in line with forecasts — sentiment is stabilising at deeply depressed levels.

UK Autumn Budget – Gilt Positive

The UK’s fiscal update was received favourably by fixed-income markets:

Fiscal stance remained contained

Long-dated gilt issuance was sharply reduced, easing duration pressure

Fiscal buffer lifted to ~£22bn, enhancing credibility

UK gilt curves tightened modestly as investors welcomed the consolidation.

🇨🇳 China

China’s November PMIs delivered mixed signals:

Official NBS Manufacturing PMI: 49.2, slightly above October (49.0) but marking the eighth consecutive month of contraction.

The improvement was marginal, with demand remaining weak and price competition intense.RatingDog Manufacturing PMI: 49.9 (vs 50.6 prior), missing expectations of 50.5.

Output and new orders were stagnant, while job cuts resumed.

The readings reflect a manufacturing sector that is stabilising but not yet recovering, with export uncertainty continuing to weigh on sentiment.

🇯🇵 Japan

Japan entered the global spotlight after a material hawkish shift from the Bank of Japan.

BoJ signals December hike

Governor Ueda indicated the BoJ is ready to raise rates at the 18–19 December meeting, lifting:

Rate-hike odds: 75–80%

2-year JGB yields: to 1%, the highest since 2008

The yen strengthened on the remarks as policymakers cited:

imported inflation

currency weakness

the need to “ease off the accelerator”

A strong JGB auction further confirmed domestic appetite for yen assets, even as Takaichi’s ¥21.3tn fiscal package underscores widening fiscal–monetary divergence.

Consumer sentiment improves

Japan’s consumer confidence index rose to 37.5, the highest since April 2024, with all components improving, including:

overall livelihood

income expectations

employment outlook

durable goods purchasing intentions

Momentum continues to build in Japan’s domestic-demand recovery.

🟡 Commodities

Precious metals rallied strongly this week:

Gold +2.5%

Silver +12.5%

Drivers included:

Markets pricing an 87% probability of a December Fed cut (vs ~50% a week earlier)

Chinese silver inventories fell to the lowest level in a decade

A CME data-centre cooling failure temporarily disrupted metals data feeds, amplifying volatility

The combination of policy expectations + supply tightness continues to support bullish momentum in precious metals.

View from Genuine Impact

Markets are entering December with a complex mix of policy signals:

The US is moving toward a more dovish Fed leadership

The UK is leaning toward fiscal consolidation

Europe remains trapped in sticky services inflation

Japan is edging out of the ultra-loose era

China is stabilising, but without a clear inflection

Across asset classes, precious metals and selective AI infrastructure plays continue to offer the most attractive near-term asymmetry.

One-week market moves as of 02 Dec 2025 (Local Currencies)

Company News

CrowdStrike

CrowdStrike delivered another resilient set of results, forecasting Q4 revenue of USD 1.29–1.30 billion, well ahead of the USD 1.22 billion expected by analysts (LSEG consensus).

Momentum continues to build around the firm’s AI-enhanced cybersecurity platform, which is driving broader customer adoption and wallet share expansion.

The company also raised its full-year revenue guidance to USD 4.80–4.81 billion, while Q3 revenue and EPS came in slightly above expectations.

Shares rose ~1% in extended trading, reflecting confidence in the company’s execution and competitive positioning.

Meituan

Meituan’s food-delivery and quick-commerce segments continue to post operating losses, as the competitive “delivery war” pressures unit economics.

The market is increasingly speculating that Q3 may represent the earnings trough, with consensus expecting subsidies to continue but at a reduced scale.

Investors remain focused on the trajectory of user retention, subsidy discipline, and the pace of margin recovery heading into 2026.

Insider Portfolio Snapshot

Our portfolio holdings and performance are shown in the chart below ⬇️